Key data from Lloyd’s List Intelligence for the week ending March 10, 2024

Numbers reflect cargo-carrying vessels of 10,000dwt+. Pre-Houthi attack ‘normal’ average taken for the period November 6 - December 3, 2023.

- Total transits through the Bab el Mandeb strait were down 12% in the week ending March 10

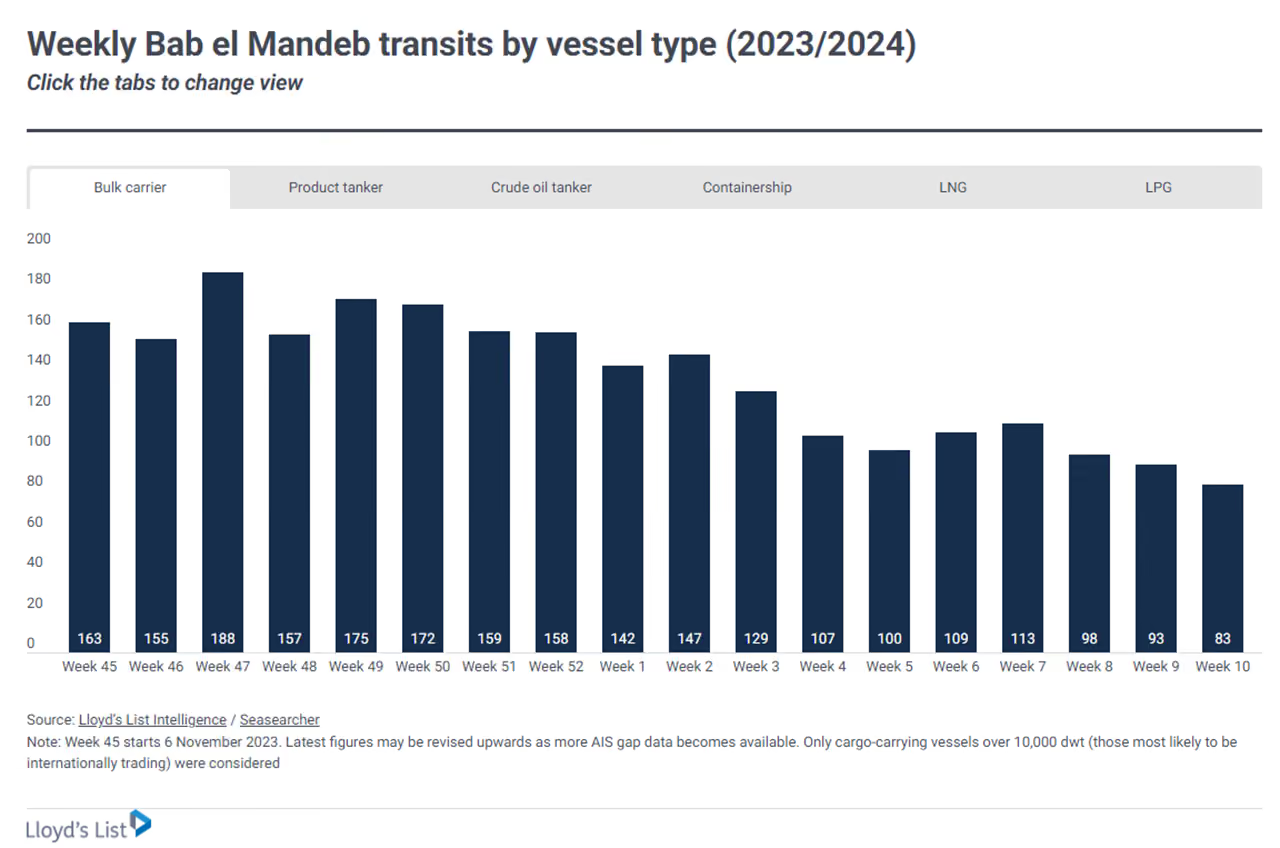

- The number of bulk carriers transiting the strait continues to slide with just 83 recorded, while no LNG carriers have risked the transit for seven weeks

- The daily average of vessels active in the Red Sea is relatively stable with 215 vessels recorded, up by around 2% on the previous week

- Suez Canal transits increased 4% compared to the previous seven days, led by notable uplifts in containerships and product tankers

- Transits by vessels around the Cape of Good Hope were down 3% compared with last week but are still up 80% against the normal average and 98% higher compared with the same week last year

There was a new low in total transit volumes of all vessel types through the Bab el Mandeb strait in the week ending March 10 (week 10 of 2024) with just 218 passings recorded. This is 60% lower than the ‘normal’ pre-Houthi attack average in vessel terms and 57% down compared with the same week last year.

In deadweight tonnage terms, the drop is 67% against the normal average.

After the significant fall seen last week, the number of bulk carriers transiting the strait continues to slide with 83 vessels recorded in week 10, down from 93 in the week ending March 3 (week 9) and 50% lower versus the normal average.

The number of crude tankers fell to 45 last week, the lowest number since 39 in week ending February 4 and 42% down on the normal average. No LNG carriers have risked passing through the strait for seven weeks.

The number of containerships increased to 40 from 34 in the week prior but this number is still 70% down on the normal average.

There was a daily average of 215 vessels active in the Red Sea in week ending March 10, which was up slightly on 210 in the previous week but considerably lower than the 382 recorded in the same week last year. The daily average has been relatively stable since week 5 when 212 vessels were recorded as active in the region.

There was a slight increase of 4% to 224 in the number of Suez Canal transits in the week ending March 10, but in terms of DWT there was little change compared with the previous seven days.

Against the normal average, Suez Canal transits breached the 50% threshold for a second time since the Houthi attacks starts – down 53% in vessel numbers and 60% in DWT. There were notable uplifts in containership transits last week – up to 39 from 29, as well as for product tankers, which were up to 36 from 19.

Cape of Good Hope passings took a slight dip in week 10, down 3% week on week but there were still more than 700 transits overall. This is up 80% compared with the normal average and 98% higher compared with the same period in 2023.

Product tanker passings around the cape were the highest since the Red Sea disruption began at 78, compared with 48 in the prior week and 255% up on the average.

For the latest insight, analysis and data, Lloyd’s List subscribers can visit our Red Sea Risk hub here.